Prediction on US Stock Market Performance (S&P 500)

.png)

.png)

Highlight

- Category: DS/ML

- Year: 2022

- Keywords: Finance, Time Series Analysis, Python

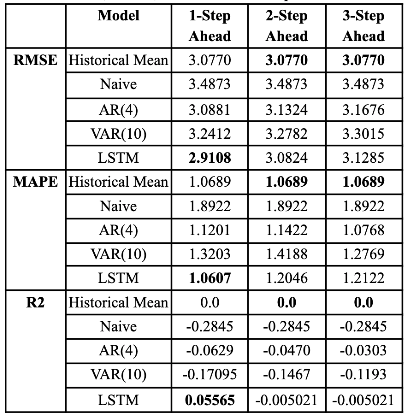

Description

In financial markets, traders and fund managers often aim to construct a simple and robust model to

predict the US S&P 500 performance. This project focuses on predicting the equity market from three

other markets — energy, bullion, and bonds. The problem of interest is to predict returns on the S&P 500

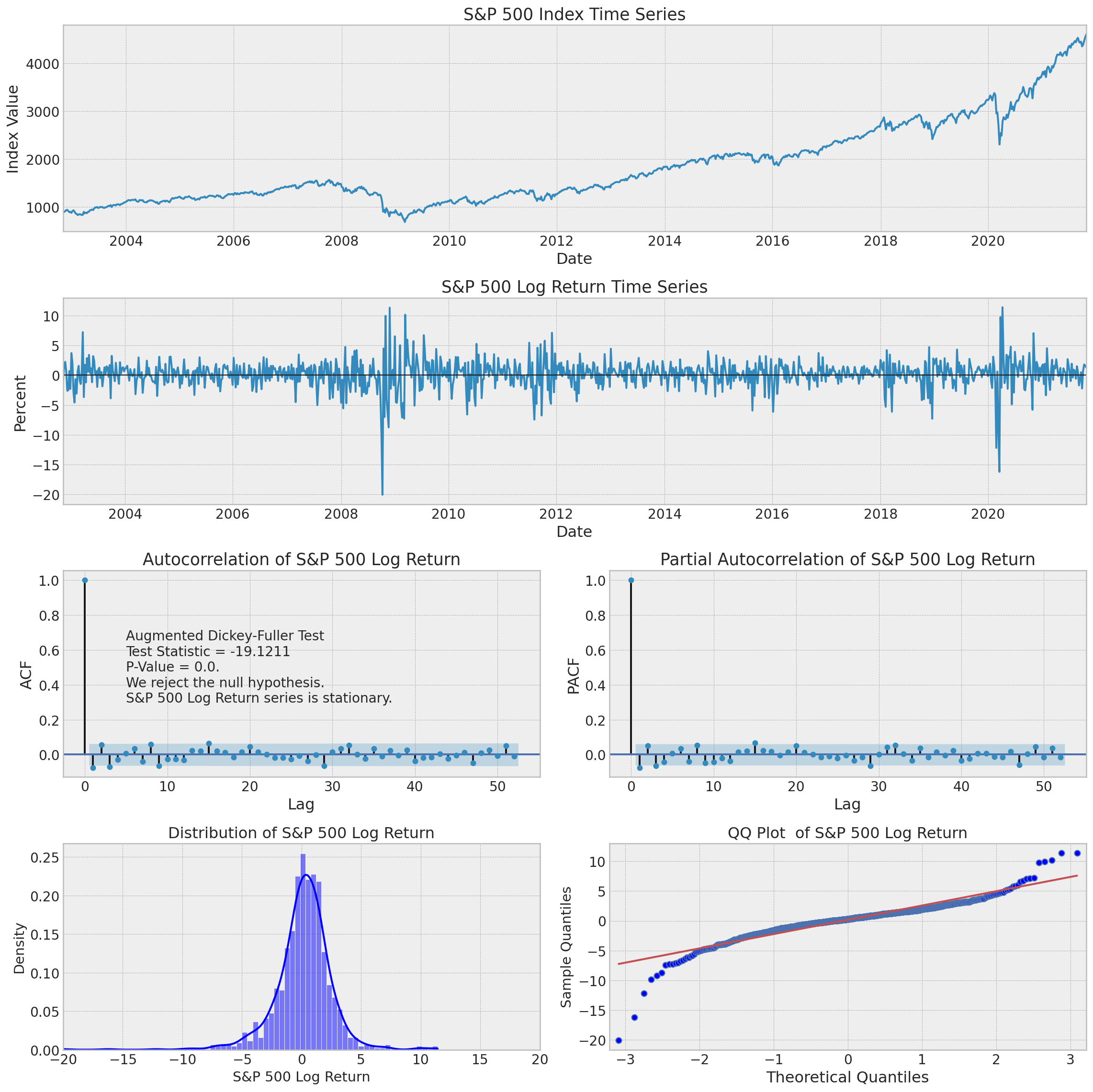

index using indicators from these three markets. EDA results show evidence of cross-correlation

and Granger causation between S&P 500 log return and other variables (crude oil futures log return,

gold futures log return, change in 3-M treasury bill yield, and change in 10Y-3M treasury yield

spread), making them promising predictors of the stocks.

For this project, the data frequency is weekly with data from November 10, 2002 to October 31, 2021

as the estimation sample, and data from November 7, 2021 to October 30, 2022 as the prediction period

(test set). The forecasting scheme is fixed (rather than recursive or rolling) and the forecasting

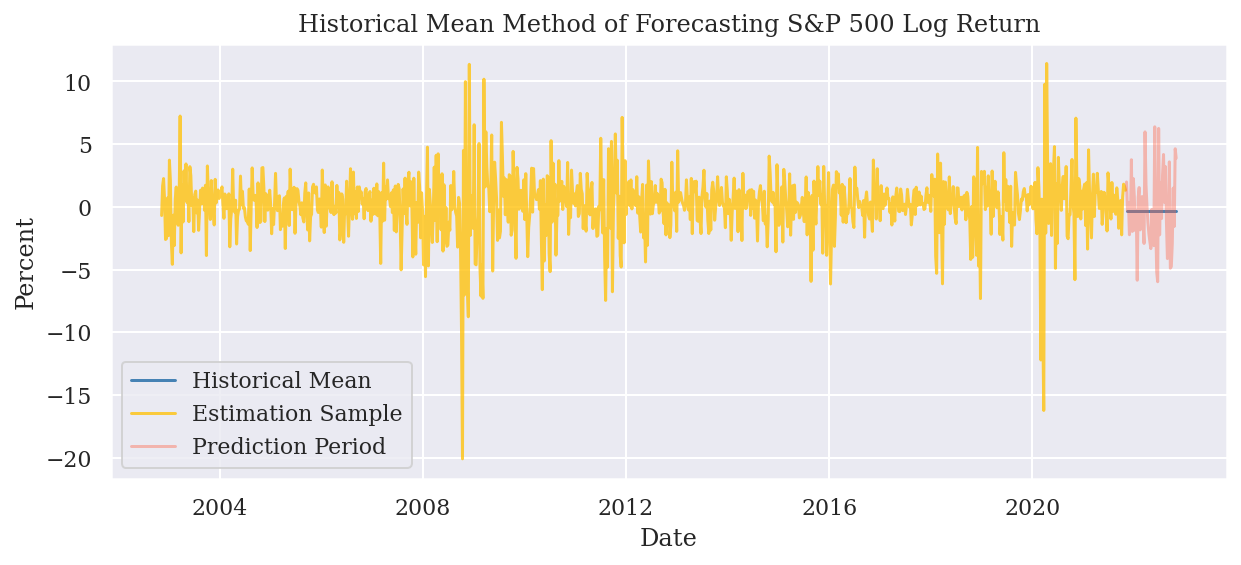

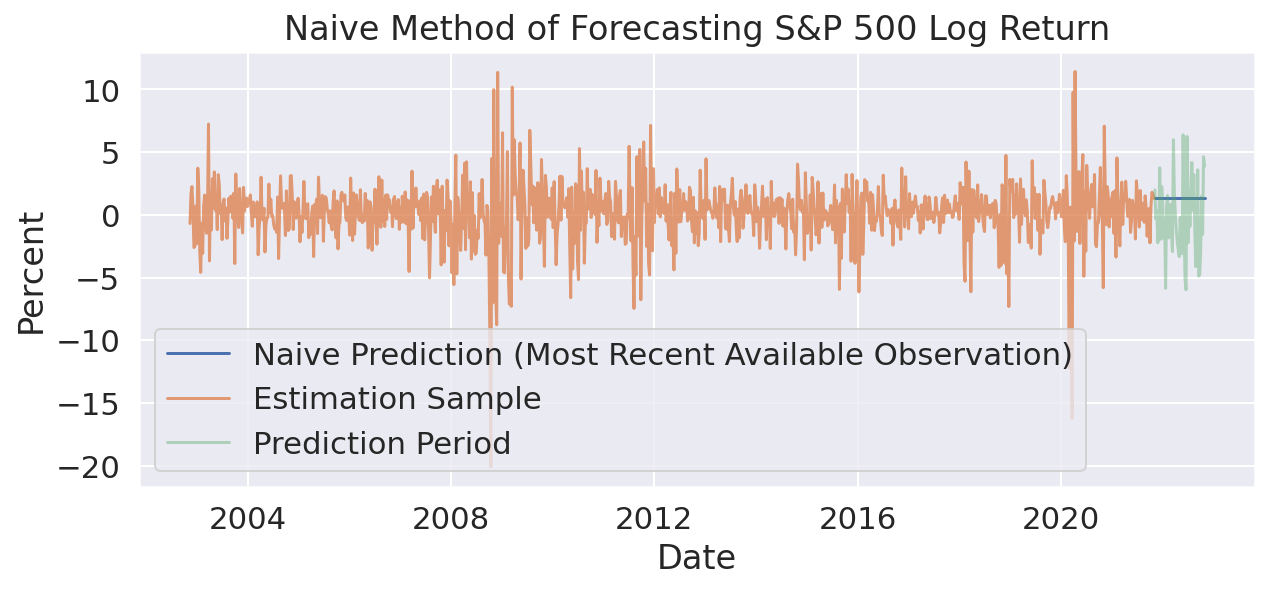

horizon is 3-step ahead. Three models are selected as the baseline: historical mean, last period naive,

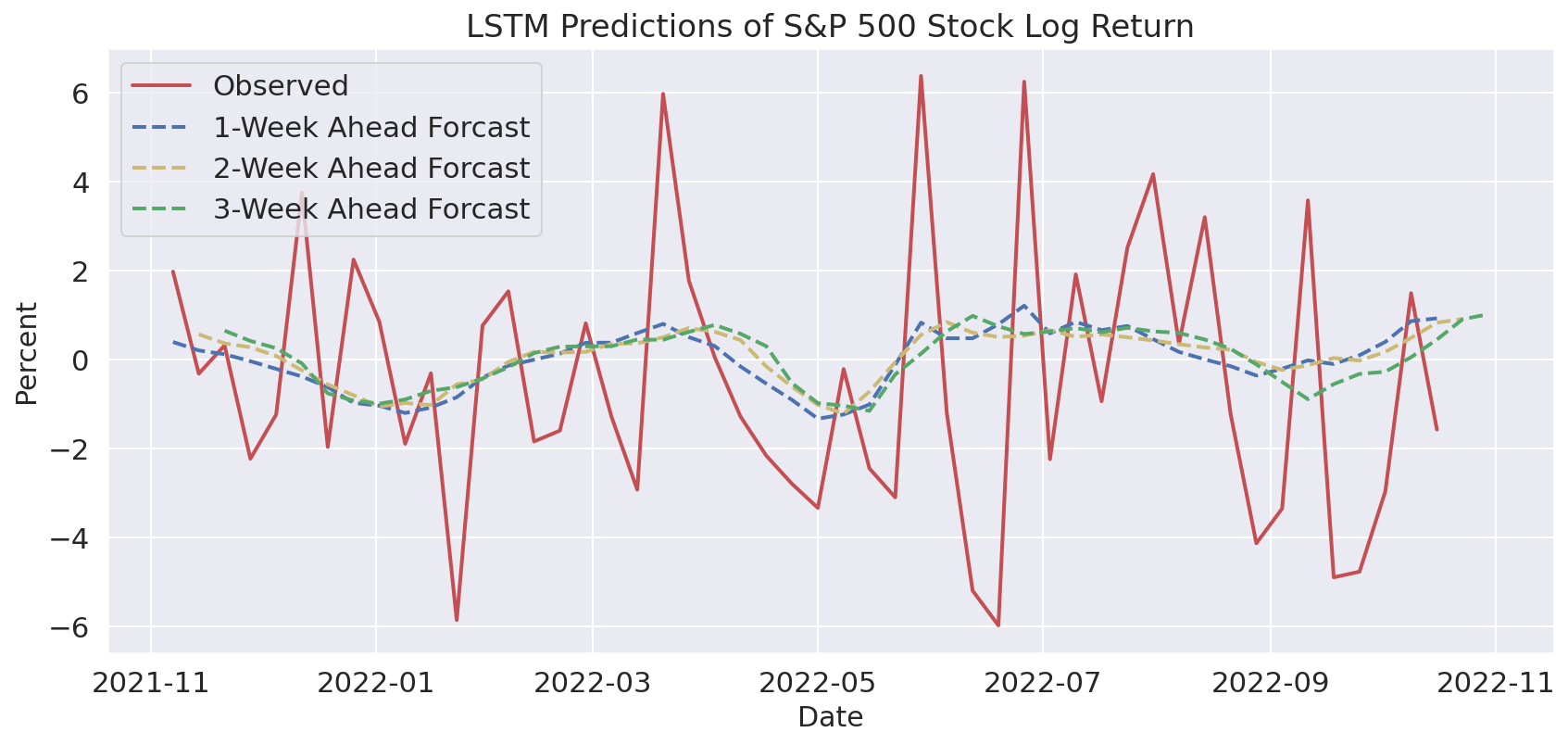

and autoregression. To improve on the baseline models, vector autoregression (VAR) and

long short-term memory (LSTM) models are built and evaluated.